I think there is a relative value opportunity in credit risk. I typically focus on equity opportunities but I think this one has the potential to be big enough to branch out to the fixed income asset class. My background is in equity derivatives, so I understand a little about the market's ability to price risk.

With long-term risk-free rates at historic lows, investors are taking on increasing amounts of credit risk without being properly compensated. People need yield and as a result are buying lower quality credits. This is happening all across the credit curve. Treasury investors are buying high-grade credits, and high-grade credit investors are moving towards high-yield. Risky credits are bid up relative to less risky credits. This presents a relative value investment opportunity to buy low-risk credits and sell high-risk credits. The beauty of this trade is that it has the potential to be profitable in two scenarios:

Recession. A recession would keep rates low, but would be a negative in particular for high-yield issuers. Defaults would scare investors away from high-yield, and investors would move toward high-quality credits.

Growth. If the economy shifts into high-gear and inflation picks up, the Fed will raise rates. When this happens, investors will be able to achieve yield in lower-risk credits. Investors will slowly pull money back toward investment grade bonds.

I like this trade because it has the potential to pay off no matter which direction the economy moves. This is the fundamental investment thesis for me in this latest spread trade. I asked myself some key questions, prior to making the investment:

1. What should timing be?

2. What are the risks here?

3. What is the best vehicle to get involved in this trade?

Timing is critical in any investment. If you time it wrong you can be sitting on a bad trade for a long time. Even Paulson’s “$15 Billion Dollar Trade” against sub-prime mortgages was in the red before it paid off. Here, shorting junk bonds has a high cost-of-carry (around 6% per year). The cost of timing it wrong can be pretty high.

Risks. The investment is profitable in both bull and bear markets. The biggest risk is that nothing happens in the market. In that case I will pay the cost-of-carry for an extended period of time before my trade is profitable.

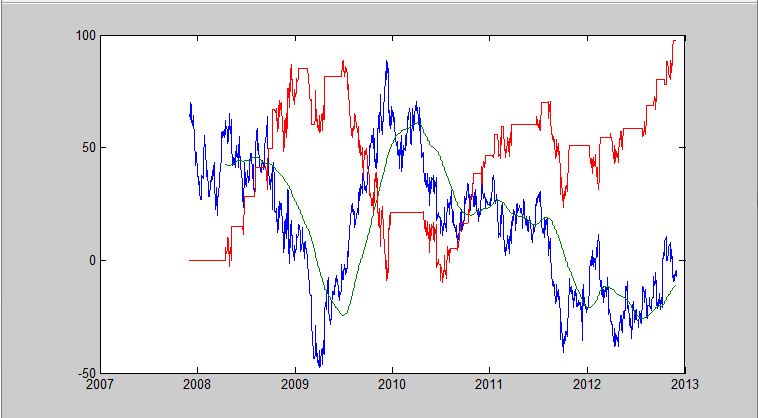

Trading Vehicle. This is an important question since it impacts my economics significantly. That said, I am sure there are many vehicles to profit from this opportunity. I don’t want to bet on specific bonds, but rather the overall market. With my typical focus on equities, I naturally look to the ETF market. Specifically, $LQD is an ETF that tracks the performance of the investment grade bond space. $HYG tracks high-yield. Both are liquid iShares ETF’s with tight bid-offers. $LQD is yielding around 3% and $HYG around 6%. With bonds, we trade pairs using the concept of duration-neutral to insulate us from the impacts of interest rate changes. $LQD has an average duration of 7.7 and HYG 3.9. Therefore I choose the ratio 1 x 2. Here is a chart of the spread 1*LQD-2*HYG. As you can see, it tends to spike higher during credit crisis times, and trend lower as rates decline. Given that $HYG has only been trading since 2007, there is not enough history to see performance during high and low interest rate regimes.

I am monitoring this spread to try to determine a good time to enter the trade long. I am also considering other trading vehicles.

What do you think of the credit markets?

Written by Jennifer Galperin. Follow me on Twitter and Stocktwits.

Jennifer Galperin

Jennifer Galperin