Trading With Python - Online Course to Boost Your Bottom Line

Jennifer Galperin

Jennifer Galperin- Update 4/17/2013. This course has started and it is closed to new applicants.

Many of you know me as a quantitative trader, blogger, and webinar host. Some of you know that I studied Engineering at MIT. I have worked a bit with computer programming and I certainly understand the power of computers to crunch huge amounts of data.

In trading, there are millions of potential trades and many different ways to evaluate each trading opportunity. Obviously this process can be improved using the data crunching power of computer programming. Of course, the idea of learning to program can be daunting. There is a steep learning curve associated with programming. That is why I am excited for an upcoming course given by fellow Bigger Capital trader and programmer Jev Kuznestov. Jev’s course is scheduled to start in April, and it will help traders learn programming as applied to quantitative trading. I have personally worked with Jev on several occasions, and I know he is a smart, experienced programmer who knows his stuff. He is also a great trader. I plan to attend the course to get up to speed on Python and learn from Jev’s expertise.

The main goal of this course is to help a trader to become a quant. It will teach how to get and process incredible amounts of data, design and backtest strategies and analyze trading performance.

The course gives you maximum impact for your invested time and money. It focuses on practical application of programming to trading rather than theoretical computer science. The course provides you with the best tools and practices for quantitative trading research, including functions and scripts written by expert quantitative traders. The course will pay for itself quickly by saving you time in manual processing of data. You will spend more time researching your strategy and implementing profitable trades.

The course will span 4 weeks, each week will start with a screencast. There will be required reading material plus example code (see example here) for further study. At the end of the week there will be a live online Q&A session.

Course fee: $350

Course material: Python for Data Analysys by Wes McKinney

Prerequisites:

- Google account

- Some basic experience with programming ( if you have no experience at all, this is a good place to start.)

Course outline:

Week 1: Getting started Python: a tool for almost any task Setting up Python environment Python language essentials Dates and times.

Week 2: Data crunching basics Introduction to NumPy (scientific and data analysis tools) Plotting with matplotlib Introduction to Pandas (data analysis package).

Week 3: Managing data Reading and writing CSV files Reading and writing excel files Getting data from the web (Yahoo finance, CBOE) Building a database with SQLite.

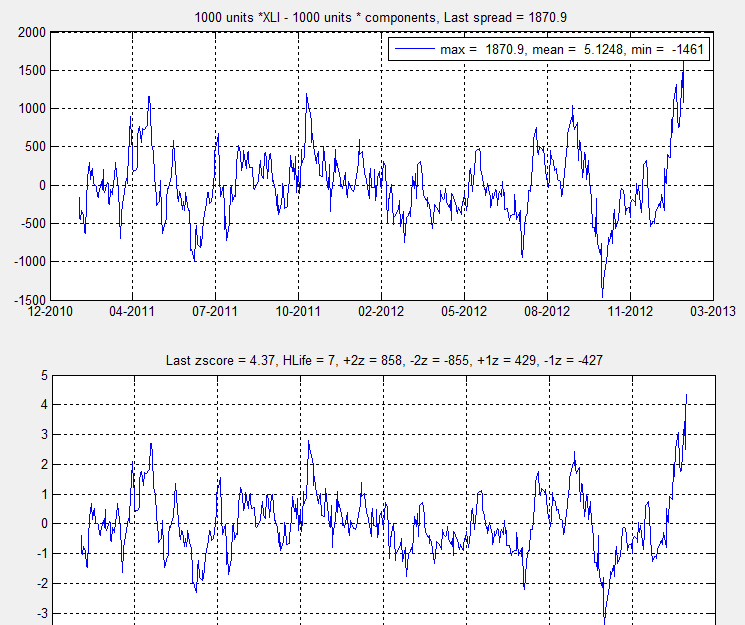

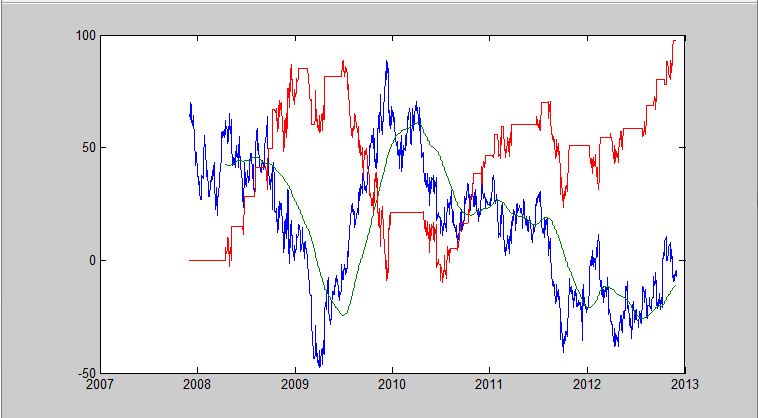

Week 4: Researching trading strategies Backtesting a single instrument (price,position & pnl) Performance measurement: common metrics (sharpe, maxDD) How to build a spread (vxx-vxz example, automatic hedge ratio calculation) Pattern matching example

An example of a screencast demonstrating strategy backtest: