We are hearing a lot of chatter about the Plug Power ($PLUG) offering that took place last week, and a lot of it is very negative in our opinion. Our first thought, like many investors, was: "Why can't they just get to profitability without raising capital?"

Once the emotional jolt lapsed we thought about it a little longer and came up with an explanation.

The answer is that they can get to profitability without this latest round. They are growing bookings, sales, and revenues ahead of plan. A plan that calls for profitability in the 2014 fiscal year. But when we invest capital we want our return to be MAXIMIZED according to the opportunities facing the company. And we think PLUG management wants that too. This is the management team that created the "GenKey" solution which simplifies the hydrogen solution for customers and anchors the PLUG solution deeper at customers sites. The customers love it.

This customers' delight is guiding PLUG to seize the amazing opportunities for growth. To name a few (Source 8-K filed 4/23/2013):

• Grow sales force to address increasing demand for the Company’s products.

• Invest in expanding into new markets, including JV's in Europe and Asia.

• Invest capital to improve vertical integration.

• Complete opportunistic acquisitions for vertical or horizontal growth.

• Focus on hydrogen generation and distribution opportunities.

• Research and develop new markets, e.g. TRUs and range extenders, plus whatever additional / adjacent applications become feasible in the near future.

With these exciting opportunities for investment, they have a choice to make. They can decide which of these "children" to feed with the capital they have, or they can raise equity capital to feed each project as much as necessary to succeed.

Now, Andy Marsh is a fairly conservative executive, and we don't think he would raise capital unless he had a real, concrete, near-term opportunity to deploy it. The JV that is in the works with Hyundai in Asia might require a capital injection from both companies. Would you prefer PLUG reject the JV opportunity in Asia for lack of available capital? Should PLUG neglect its fledgling business in Europe, a market that is much bigger than the US for PLUG products, because it lacks appropriate capital to fund this business? If the company finds an opportunity to acquire strategic technologies on the cheap by purchasing small companies with complementary portfolios of patents, are you saying postpone and open the door for a competitor?

Plug Power is building its arsenal for the battle of world domination of the hydrogen business. The company has cracked the hydrogen code and it has a significant time lead over potential entrants. Now is not the time to futz around or take things slow. PLUG must strike now. These are the opportunities of a lifetime and it makes sense to capitalize on them even if it means the stock price suffers a little bit in the short term. Go for the jugular PLUG, you will not have a second chance!

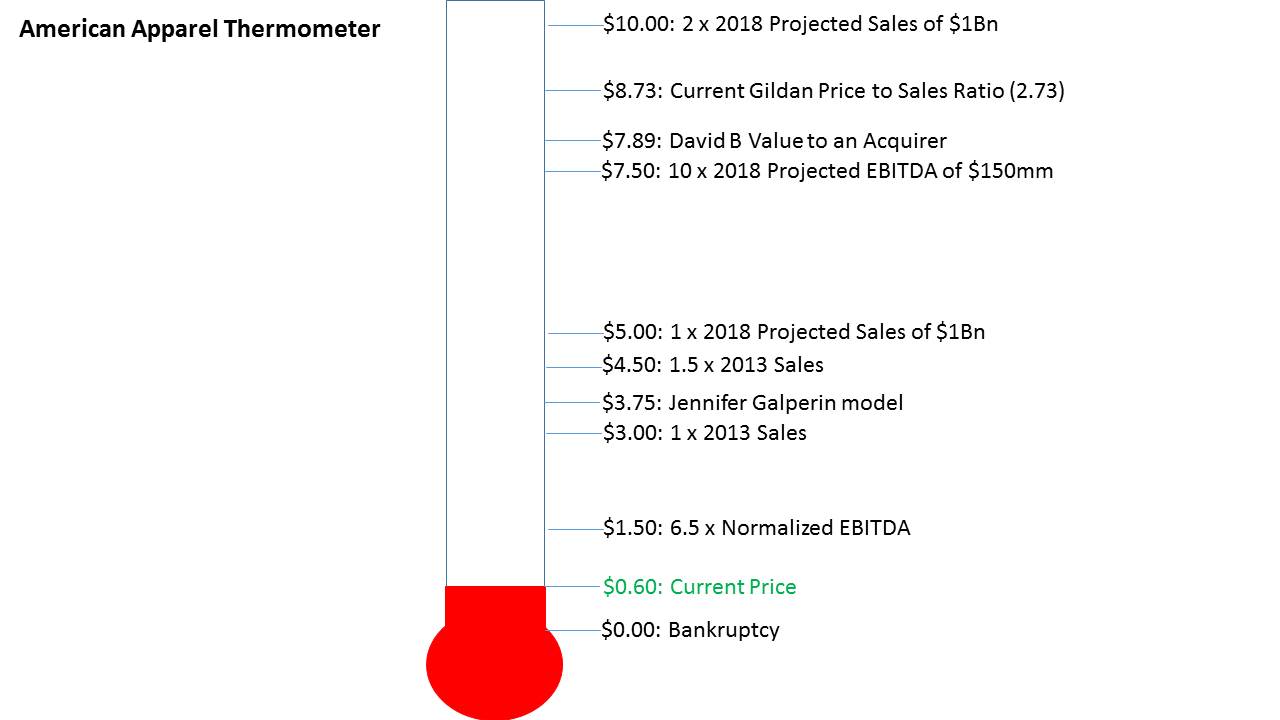

Written by Jennifer Galperin and Michael Bigger.

Disclaimer: Bigger Capital, LLC, Bigger Capital Fund, LP, Bachelier, LLC and the Bigger family hold a very large stake in Plug Power. We have participated in the latest stock offering and we purchased call options as of 4/28/2014. We have a very long term horizon that extend much further than the average investor's time horizon. These high growth situations are often not suitable for most investors since they are extremely volatile and it can take decades to realize their full potential. Take our opinions with a grain of salt and do your homework.

Michael Bigger

Michael Bigger